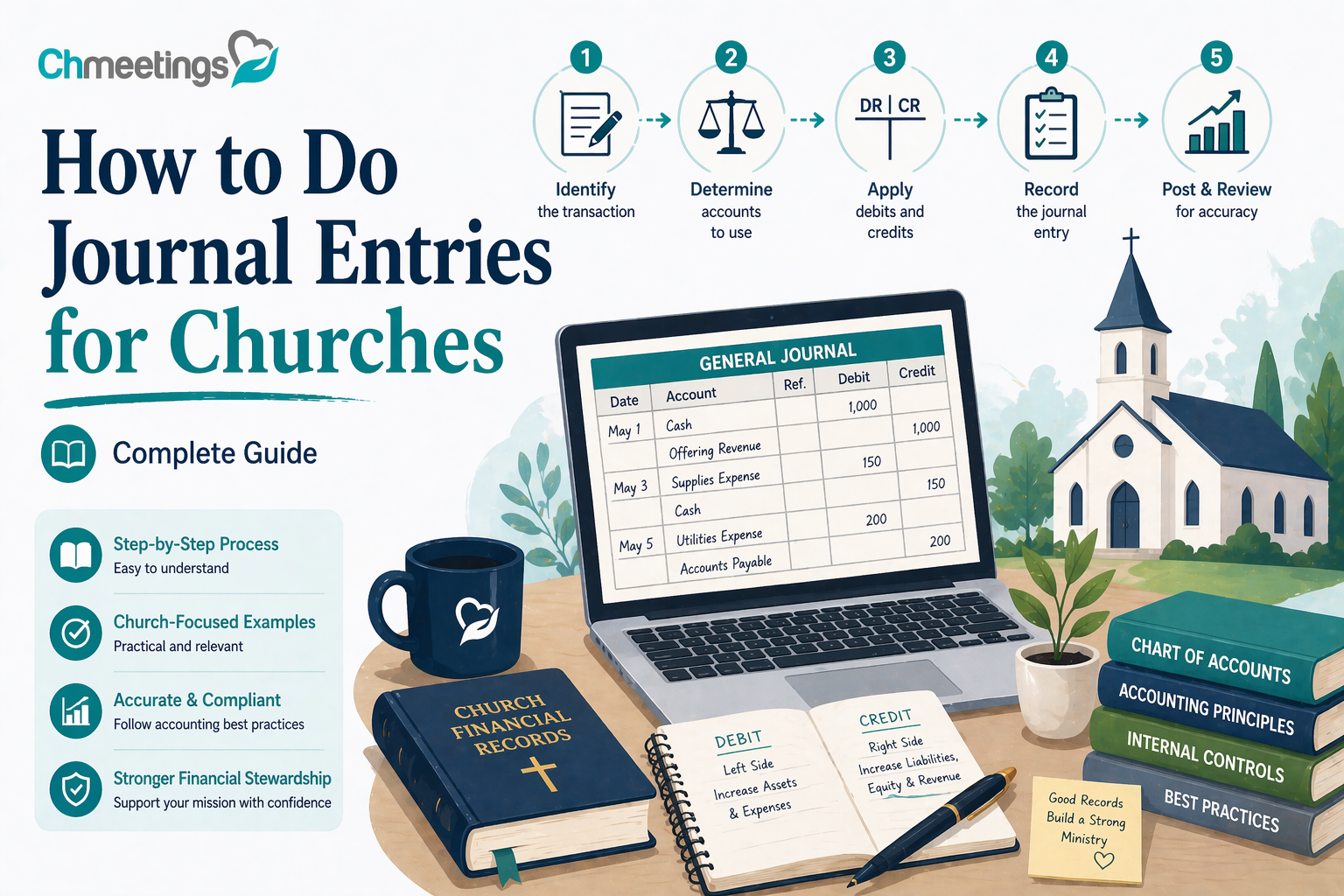

- Why Journal Entries Matter For Churches

- How Does Fund Accounting Affect Entries?

- What Should Be In Your Chart Of Accounts?

- How To Record Donations And Giving

- How To Enter Payroll And Related Costs

- How To Handle Transfers And Reclassifications

- How To Post Adjusting And Year End Entries

- How To Reconcile Accounts Regularly

- How To Use Church Accounting Software

- What Internal Controls Prevent Errors

- How To Close The Month And Review Reports

- Which Common Mistakes To Avoid

- Journal Entry Playbook And Templates

- FAQs

Why Journal Entries Matter For Churches

Journal entries are the building blocks of your church’s financial story. They record every transaction, which keeps your books accurate, helps you follow donor intent, and makes month-end and annual reporting possible. Good entries reduce confusion during audits, speed up reconciliations, and free leaders to focus on ministry instead of chasing numbers.

What Journal Entries Show

A journal entry shows the date, accounts affected, debit and credit amounts, and a short description of why the entry exists. For churches, the most common lines are cash, bank deposits, contribution revenue, restricted funds, expenses, and transfers between funds. Together those lines show where money came from, how it was used, and whether any donor restrictions remain.

How They Support Donor Trust

Clear, consistent entries show donors their gifts were handled responsibly. When you can produce giving records and fund balances quickly, donors feel confident you honored their intent. That trust makes repeat giving and larger commitments more likely. Keep entries linked to documentation, like deposit logs and donor acknowledgments, so you can answer questions without digging through spreadsheets.

How Does Fund Accounting Affect Entries?

Fund accounting changes the way you record transactions because you’re tracking purpose, not just profit or loss. Each entry must point to a fund or purpose so restricted gifts stay protected and ministry leaders get accurate budget reports. That affects how you categorize revenue, record transfers, and present financial statements.

Track Restricted Versus Unrestricted Funds

When a gift is restricted, your entry needs to preserve that restriction. Typical approach on receipt is:

- Debit bank or cash

- Credit temporarily restricted revenue or a restricted fund liability

When the funds are spent for the donor’s purpose, you record a release:

- Debit restricted revenue release

- Credit expense or transfer the amount into the operating fund

Unrestricted gifts simply credit general operating revenue on receipt. The key is consistent tagging so you can pull fund balances at any time.

Report Fund Balances By Purpose

Don’t just report a single cash number. Produce a fund balance schedule that lists each fund, beginning balance, inflows, outflows, and ending balance. That schedule answers common questions, like how much is available for building repairs versus missions. It also simplifies board meetings and stewardship reports.

Example Fund Entry Workflows

- Weekly offering: count and batch by fund, prepare deposit slip, enter bank deposit, post journal entry debiting bank, credit each fund’s contribution account. Reconcile deposit to bank.

- Restricted gift received online: platform posts gross deposit to bank, record fee as expense or contra-revenue, credit restricted revenue account, document donor restriction.

- Drawdown from building fund: create a transfer journal entry moving cash from Building Fund to Operating Fund, then post expense entries when bills are paid.

Document each step and attach supporting files to the entry, so anyone reviewing can follow the chain from donation to expense.

What Should Be In Your Chart Of Accounts?

A chart of accounts should be simple enough to manage but detailed enough to track ministry priorities. Organize accounts by assets, liabilities, net assets or equity, revenue, and expenses, then add fund and program tags. Consistency matters more than complexity.

Accounts Every Church Needs

At minimum include:

- Assets: Cash in Bank, Petty Cash, Prepaid Expenses, Fixed Assets

- Liabilities: Accounts Payable, Payroll Liabilities, Deferred Revenue

- Net Assets: Unrestricted Net Assets, Temporarily Restricted Net Assets, Permanently Restricted Net Assets

- Revenue: Tithes, Offerings, Online Giving, Grants, Fundraising Income

- Expenses: Payroll, Facilities, Worship, Children’s Ministry, Outreach, Administration

Keep account names short and self-explanatory. If someone on the team asks what an account is for, the name should answer.

Map Giving Types To Accounts

Map common giving types to specific revenue accounts so reporting is meaningful. For example:

- Tithe → Tithes income account

- General offering → Offerings income account

- Building fund → Building fund revenue

- Missions gift → Missions revenue

If a gift arrives with multiple designations, split the journal entry so each portion posts to the correct account. That makes year-end statements and donor receipts accurate.

Use Departments And Programs

Add department or program tags to track spending by ministry, not just by account. Tag wages and program expenses to Worship, Youth, Outreach, etc. That lets you produce program-level P&Ls and evaluate ministry impact. Many church management apps let you automate account and tag mapping, so routine gifts and expenses post with the right classifications every time.

How To Record Donations And Giving

Recording donations consistently preserves donor intent and simplifies reporting. Use a repeatable process: document the gift, choose the correct account and fund, record the entry, and attach supporting paperwork or scans.

Record Cash Plate Gifts

Best practice:

- Count with two unrelated people, log amounts by fund

- Prepare deposit and post bank deposit

Journal entry example:

- Debit Bank

- Credit Contributions – Plate (or relevant fund accounts)

Attach the count sheet and deposit slip to the entry so auditors and pastors can verify amounts.

Post Online Giving And Fees

Online platforms usually deposit net amounts, while fees were deducted before deposit. Your entry should show gross revenue and fees, or show net revenue with a separate fees expense, depending on your reporting preference. Two common approaches:

Option 1, gross revenue:

- Debit Bank for net deposit

- Debit Bank Fees or Processing Fees expense for fees amount

- Credit Contributions Revenue for gross donation amount

Option 2, net revenue:

- Debit Bank for net deposit

- Credit Contributions Revenue for net amount

- Document fees separately for transparency

Whichever method you choose, be consistent and reconcile platform reports to bank deposits. A church management app can simplify this by importing gifts and matching fees.

Record Pledges And Pledge Payments

Pledges are commitments, not cash, so treat them carefully. Many churches track pledges as memorandum records and do not record receivable unless pledges are legally enforceable. If you record a receivable:

- On pledge: Debit Pledge Receivable, Credit Pledge Revenue or Temporarily Restricted Revenue

- On payment: Debit Bank, Credit Pledge Receivable

If you prefer simpler bookkeeping, track pledges in your pledge module and record revenue when payments arrive.

Account For Restricted And Designated Gifts

When a donor restricts a gift:

- On receipt: Debit Bank, Credit Temporarily Restricted Revenue or Restricted Fund

- When spent for the restriction: Debit Restricted Revenue Release, Credit Expense or transfer to operating accounts

Always record the donor restriction in the entry memo and keep donation agreements or communications attached. That documentation proves intent if questions arise.

Log In Kind Donations And Fair Market Value

Noncash gifts must be recorded at fair market value on the date received. Common examples are donated equipment, furniture, and professional services that meet recognition criteria.

Typical entries:

- For donated equipment: Debit Fixed Assets at fair market value, Credit Contributions Revenue

- For donated supplies used immediately: Debit Expense, Credit Contributions Revenue

Document how you arrived at fair market value, include appraisals or donor estimates, and follow local tax guidance for reporting. For donated services, record only when the services create or enhance nonfinancial assets or meet specific recognition rules.

If you want, I can convert any of these examples into ready-to-use journal templates or sample entries tailored to your church’s chart of accounts. I can also show how a church management app can automate mapping and reporting for donations.

How To Enter Payroll And Related Costs

Record Gross Payroll And Net Pay

Record payroll in two clear steps, gross then net, so your expense and liability accounts stay accurate. When payroll is earned but not yet paid:

- Debit Salaries and Wages Expense for gross pay.

- Credit Federal Withholding Payable, State Withholding Payable, FICA Withholding Payable, and any other employee-withheld liability accounts for tax and benefit deductions.

- Credit Net Payroll Payable (or Cash if you pay immediately) for the net amount due to employees.

When you run payroll and actually pay staff:

- Debit Net Payroll Payable.

- Credit Bank or Cash.

Example entries

- Payroll earned: Debit Payroll Expense $10,000; Credit Withheld Taxes Payable $2,500; Credit Retirement Withholding Payable $500; Credit Net Payroll Payable $7,000.

- Payroll paid: Debit Net Payroll Payable $7,000; Credit Bank $7,000.

Always attach the payroll register and timesheets or approval notes to the journal entry, so anyone reviewing can see how the amounts were calculated.

Post Payroll Tax Liabilities

Separate employee withholdings from employer tax obligations, they require different journal entries and remittance timing. At payroll run, record employee withholdings as liabilities. For employer payroll taxes, book both the expense and the liability:

- When payroll is recorded: Debit Payroll Tax Expense (employer share) for payroll taxes owed by the employer, Credit Payroll Tax Payable.

- When you remit taxes: Debit the relevant liability (Withheld Taxes Payable and Payroll Tax Payable), Credit Bank.

Example

- Record employer tax: Debit Payroll Tax Expense $800; Credit Payroll Tax Payable $800.

- Remit taxes: Debit Payroll Tax Payable $800; Debit Withheld Taxes Payable $2,500; Credit Bank $3,300.

Keep a tax remittance calendar and copies of filings. Mistimed or missing payments create penalties that must be tracked and recorded.

Handle Benefits And Retirement Contributions

Treat benefits and retirement the same way you treat payroll deductions, split into employee-withheld amounts and employer-paid amounts.

- Withholdings: at payroll, Credit Retirement Withholding Payable or Health Insurance Payable for employee contributions.

- Employer match: Debit Benefits or Retirement Expense, Credit Employer Benefits Payable.

- When you pay the provider: Debit the payable, Credit Bank.

If benefits are invoiced monthly by an insurer, post the vendor invoice to capture the expense and liability, then reconcile the invoice to the payroll withholdings when remitted. Keep plan documents and vendor statements attached to entries so auditors can verify eligibility and amounts.

Manage Staff Reimbursements And Stipends

Reimbursements are expense reimbursements, not income, so they need receipts and proper approvals.

- For direct reimbursements: Debit the appropriate expense (Travel, Meals, Supplies), Credit Bank or Petty Cash.

- For advances: when you issue an advance, Debit Staff Advances (asset), Credit Bank. When the employee submits receipts, Debit Expense, Credit Staff Advances for the settled amount. If receipts are missing, follow your policy before clearing the advance.

Stipends require tax classification. If a stipend is payroll subject, process it through payroll so withholdings are handled. If it is a nonemployee honorarium, record as Other Expense and follow reporting rules for 1099s if applicable.

Always retain receipts and an approval memo with each reimbursement entry, and have a consistent policy for advances versus reimbursements.

How To Handle Transfers And Reclassifications

Post Interfund Transfers

Interfund transfers move cash or balances between funds, they are not revenue or expense. Record the movement so fund balances remain accurate.

- Moving cash from Building Fund to Operating Fund: Debit Bank, Operating Fund; Credit Bank, Building Fund (or use fund-specific cash accounts).

- Note the purpose and attach board approval or donor release documentation.

Example

- Transfer $5,000 from Building to Operating: Debit Cash – Operating Fund $5,000; Credit Cash – Building Fund $5,000.

Tag transfers by fund and program so the finance team can report fund-level cash positions without manual reconciliations.

Reclassify Funds When Restrictions Lift

When donor restrictions are satisfied, reclassify net assets rather than treating the change as new income.

- Record the release from restriction: Debit Temporarily Restricted Net Assets, Credit Unrestricted Net Assets or Revenue Released from Restrictions.

- If cash also moves between funds, post the interfund transfer separately.

Example

- Donor-restricted gift released for building repairs: Debit Temporarily Restricted Net Assets $10,000; Credit Released from Restrictions $10,000. Then, if cash moves, post the cash transfer entry.

Keep donor agreements and ministry approvals attached, and ensure the finance committee signs off on releases.

Move Between Operating And Savings Accounts

Transfers between bank accounts are balance sheet entries only, used to manage cash flow and reserves.

- To move money from checking to savings: Debit Savings Account, Credit Checking Account.

- Reconcile monthly to bank statements and document the reason, for example, reserve funding or emergency cushion.

Set approval thresholds for who can authorize transfers, and schedule regular reviews of cash balances so transfers match ministry priorities.

How To Post Adjusting And Year End Entries

Accruals And Prepaid Adjustments

Adjusting entries align your books to the accrual basis, recognizing expenses when incurred and revenue when earned.

- Accrual for unpaid utilities at month-end: Debit Utilities Expense, Credit Accrued Liabilities.

- Recognition of prepaid insurance each month: Debit Insurance Expense, Credit Prepaid Insurance.

Run a monthly checklist of common accruals, such as payroll, utilities, and grant expenses, and reverse short-term accruals in the following period if appropriate.

Record Depreciation And Amortization

Depreciation spreads the cost of fixed assets over their useful lives, you do not change the asset cost.

- Monthly or annual entry: Debit Depreciation Expense, Credit Accumulated Depreciation.

- For intangibles, debit Amortization Expense, Credit Accumulated Amortization.

Maintain a fixed asset schedule showing purchase date, cost, useful life, method, and accumulated depreciation, and attach it to the journal entry for transparency.

Make Year End Cleanup Entries

Year end is a time to tidy, not invent numbers. Typical cleanup work includes:

- Confirming accruals and clearing those that should not carry forward.

- Reviewing receivables and establishing allowances for doubtful accounts.

- Reclassifying temporarily restricted net assets that were released.

- Recording final adjustments for payroll, benefits, and taxes.

Close out nominal accounts as required by your reporting policy, prepare schedules for auditors, and have the finance committee review significant adjustments. Create templates for recurring year-end entries to reduce errors next year.

How To Reconcile Accounts Regularly

Bank Reconciliation Steps

A reliable reconciliation process prevents surprises.

- Pull the bank statement and the general ledger cash balance for the same date.

- Mark cleared items on the ledger against the bank statement.

- Identify outstanding checks and deposits in transit, and record them as reconciling items.

- Post bank service fees, interest, and returned items to the ledger.

- Adjust the ledger with journal entries for any bank charges or errors, then confirm the adjusted book balance equals the bank ending balance.

Reconcile monthly at minimum, more often if your church processes many transactions.

Match Merchant And Giving Platform Deposits

Payment processors and online giving platforms often batch and net deposits, which complicates reconciliation.

- Compare the platform deposit report to the bank deposit and your gift records line by line.

- Record processing fees either as a separate expense or as a contra-revenue, depending on your reporting preference, and be consistent.

- Consider using an Undeposited Funds or Clearing account to hold individual gifts until the bank deposit posts, then move the total from the clearing account to cash.

A church management app can import gifts and help match platform deposits to gifts automatically, saving hours of reconciliation work and reducing errors.

Resolve Unclear Or Unmatched Transactions

When a transaction doesn’t match, use a clear process to resolve it.

- Trace the item to a receipt, deposit slip, or platform report. Attach whatever you find to the journal entry.

- If information is missing, contact the bank or processor for details.

- Post the amount temporarily to a Suspense or Clearing account, but set a deadline to resolve it. Long-term suspense balances hide problems.

- Once traced, move the amount to the correct account with a reversing entry from the suspense account.

Document investigations and final resolution steps, then review recurring issues to improve controls and avoid repeats.

How To Use Church Accounting Software

Manual Entry Versus Software Entry

Manual entries, like typing into a spreadsheet, work in a pinch but invite errors and version control headaches. Software entry centralizes records, enforces validation rules, and remembers account mappings so common transactions post consistently. For churches, that consistency protects restricted funds and simplifies donor reporting. Use manual entries only for rare, nonrecurring items or when you need a temporary suspense posting, then convert those into formal journal entries in your system.

Entering Journal Entries Online

When you enter journal entries online, start with a clear memo that includes the why, who approved it, and links to supporting files. Break multi-purpose transactions into separate lines so each fund and revenue account stays accurate. If your team uses a church management app, import giving batches or vendor invoices directly when possible to avoid double entry. Always preview the balanced debit and credit totals before posting and use a posting date that matches the underlying activity, not just the date you entered it.

Exporting And Saving PDF Templates

Create a reusable PDF template for recurring entries, like monthly rent, depreciation, or payroll clearing. Save the PDF with a naming convention that includes period and purpose, for example, “2026-03_Depreciation_Template.pdf.” Store templates in a shared folder and attach the template or a filled copy to the journal entry so reviewers see the calculation. If your church uses cloud software, export the posted entry or a printable report to PDF at close, then archive it with bank statements and payroll registers.

What Internal Controls Prevent Errors

Segregation Of Duties Best Practices

Split critical tasks across people, not one overworked volunteer. Typical segregation: one person enters journal entries, another reviews and approves them, a third reconciles bank statements. Keep single-person exceptions documented and temporary. For small staffs, rotate responsibilities periodically and require secondary approvals for high-value or fund transfers.

Approval And Documentation Standards

Set approval thresholds and a clear sign-off process, for example, any journal entry over $1,000 requires two approvals. Require source documents for every entry, such as deposit slips, invoices, donor emails, or board minutes releasing restricted funds. Keep approval stamps, digital signatures, or audit comments on the entry so reviewers can see the decision trail without emailing back and forth.

Maintain An Audit Trail For Each Entry

Attach receipts and supporting files directly to each journal entry and record who made and who approved the post. Use immutable timestamps where possible, and never overwrite an entry without a reversing entry and new post. An audit trail speeds audits and builds donor confidence, because you can show the exact paper trail from gift to expense.

How To Close The Month And Review Reports

Monthly Close Checklist

Close the month with a short checklist: post all cut-off journal entries, record accruals and prepaid amortizations, reconcile bank and merchant accounts, clear suspense accounts, confirm payroll liabilities, and review restricted fund releases. Mark the accounting period as closed in your system to prevent after-the-fact edits. Save a zip of the month’s PDFs, reconciliations, and supporting schedules for the finance committee.

Key Reports To Run And Check

Run the trial balance, statement of activities by fund, balance sheet, bank reconciliation report, and pledge versus receipts report. Look at aged payables and an expense detail for large variances. If you use a church management app, export the giving batch report and compare it to the deposit total. These reports together show whether books are balanced and whether fund restrictions were respected.

Compare Actuals To Budget

Pull a budget versus actuals report by fund and program, then investigate variances above an agreed threshold, say 5 percent or $500. Ask program leaders to explain sustained overages or underspends and document decisions to adjust future budgets. Use the findings to reforecast cash needs and to inform stewardship conversations with the board, so budgeting becomes a tool for ministry planning, not just accounting.

Which Common Mistakes To Avoid

Misclassifying Restricted Funds

Treat restricted gifts as anything but general operating revenue and you risk breaking donor trust and creating compliance problems. When in doubt, record the gift to a restricted fund and ask for clarification. If you release restrictions, document the authority for the release and post a clear reclassification entry, so reports always show how donor intent was respected.

Forgetting To Reconcile Regularly

Skipping reconciliations lets errors compound and hides processor or bank mistakes. Reconcile bank and merchant accounts monthly at minimum. If deposits from online giving show timing or fee differences, use a clearing account so each gift and fee is traceable. Unresolved suspense balances over 30 days should trigger a review.

Lacking Supporting Documentation

Entries without receipts or notes are audit red flags and stress your volunteers. Require source documents on every material entry and attach them to the journal entry. Keep a retention schedule so older records are archived but available. If you must use a temporary entry, add a deadline to resolve it and assign ownership for follow up.

Journal Entry Playbook And Templates

Create a short playbook your team can follow, and keep a handful of ready-to-use templates for recurring transactions. A playbook reduces questions, speeds entries, and protects restricted funds. Store templates and supporting files in your shared finance folder or in your church management software so entries stay consistent and auditable.

Step By Step Entry Template

- Header fields to always complete: Date, Period, Entered By, Approved By, Source Document(s) linked.

- Memo: one sentence explaining the why, including fund or donor restriction and approval reference.

- Line items: list account, fund or tag, debit, credit, and any class or program code.

- Attachments: deposit slip, gift agreement, pledge schedule, payroll register, vendor invoice, or bank statement.

- Approval: who reviewed and date, and a short checklist confirming debits equal credits, fund designation checked, and supporting docs attached.

Example filled template for a routine deposit:

- Date: 2026-03-21

- Memo: Weekly offering by fund, counted by A. Smith and J. Cruz.

- Line 1: Bank, Operating Fund, Debit $6,400

- Line 2: Contributions – Unrestricted, Operating Fund, Credit $5,800

- Line 3: Contributions – Building Fund, Building Fund, Credit $600

- Attachments: count sheet, deposit slip, bank deposit image

- Approved by: Finance Chair, 2026-03-22

Sample Entry: Donation With Fee

Two common approaches, pick one and apply consistently.

Option A, gross revenue with fee shown separately:

- Bank, Debit (net deposit) $970

- Processing Fees Expense, Debit $30

- Contributions – Gross, Credit $1,000

Memo: Online donation, donor designated Missions, platform fee $30. Attach platform report and deposit slip.

Option B, net revenue, fees recorded separately for transparency:

- Bank, Debit $970

- Contributions – Net, Credit $970

- Processing Fees Expense, Debit $30

Memo: Same as above, note gross amount in attached platform report.

Either way, tag the contribution to the Missions fund so donor intent is preserved.

Sample Entry: Pledge Payment

If you track pledges as receivables:

- When pledge recorded (optional): Pledge Receivable, Debit $2,000; Pledge Revenue (or Temporarily Restricted), Credit $2,000.

- On payment: Bank, Debit $500; Pledge Receivable, Credit $500.

Memo: Payment against 2026 pledge, donor Smith, installment 1 of 4. Attach pledge agreement and payment remittance.

If you track pledges off ledgers and only record cash:

- On payment: Bank, Debit $500; Contributions – Pledge Revenue, Credit $500.

Memo: Same attachment set. Note which pledge batch and period for board reporting.

Sample Entry: Payroll Posting

Two-step approach keeps liabilities clear.

1) Accrue payroll when earned:

- Salaries and Wages Expense, Debit $10,000

- Employee Withholdings Payable, Credit $2,500

- Employer Payroll Taxes Expense, Debit $800

- Employer Payroll Taxes Payable, Credit $800

- Net Payroll Payable, Credit $7,300

Memo: Payroll for pay period ending 03/15/2026, attach payroll register and timesheets.

2) When payroll is paid:

- Net Payroll Payable, Debit $7,300

- Bank, Credit $7,300

- When taxes are remitted, debit the respective payable accounts, credit Bank, and attach remittance proof.

Sample Entry: Interfund Transfer

Transfers move cash between funds, they are not revenue.

Example, move $5,000 from Building Fund to Operating Fund:

- Cash – Operating Fund, Debit $5,000

- Cash – Building Fund, Credit $5,000

Memo: Board-approved transfer to cover December roofing expense, board minutes attached. Tag both lines with transfer code and who approved.

For transparency, include the authorization document and reference the purpose so reviewers can trace the reason for the move.

FAQs

How Do I Get Journal Entry PDFs?

Most accounting systems and church management apps let you print or export a posted entry to PDF. If you use desktop software, choose Print and pick Save as PDF. If you entered entries in a spreadsheet, export the sheet or print the entry area to PDF and attach source documents. Name PDFs with date and purpose, for example 2026-03_WeeklyDeposit_0321.pdf, and store them with your monthly close files.

Can Volunteers Enter Journal Entries?

Yes, with controls. Limit volunteers to data entry roles, require a different person to review and approve entries, and restrict access to sensitive accounts like payroll and bank transfers. Provide a short training checklist, require supporting documents on every entry, and set approval thresholds for higher value posts.

How Often Should Entries Be Posted?

Post giving and bank deposits weekly, more often if you receive daily online deposits. Accruals, payroll, and merchant fee adjustments can be posted each payroll or month end. Perform full reconciliations and close the period monthly. Faster posting improves transparency and reduces month-end surprises.

How Do I Record Online Giving Deposits?

Match the platform deposit report to the bank deposit, then post either gross revenue with fees separated, or net revenue with fees as an expense. A common journal for gross reporting:

- Bank, Debit (net amount)

- Processing Fees Expense, Debit (fees)

- Contributions – Gross, Credit (gross donations)

Attach the platform activity report and the bank deposit. Consider using a clearing account to hold individual gifts until the deposit posts, that makes reconciliation easier.

How Do I Correct A Mistaken Entry?

Do not delete a posted entry. Post a reversing entry dated the same period to negate the mistake, then record the correct entry with a clear memo and attachments. For material changes, get approval from the finance chair and document the reason. Keep both the reversal and corrected entry in the audit trail so auditors can follow what happened.

Which Reports Show Fund Balances?

Key reports are the balance sheet with fund breakdown, statement of activities by fund, and a fund balance schedule that lists beginning balance, inflows, outflows, and ending balance. A trial balance with fund tags and a restricted versus unrestricted net assets report are also useful. If you use a church management app, export giving and fund reports to reconcile gift detail to ledger balances.