- What Pastor Compensation Includes

- Comparing Salaries By Church Size

- Role-Based Pay Differences

- Regional And Denominational Trends

- Factors That Drive Pay Levels

- How To Calculate A Fair Salary

- Building A Formal Compensation Policy

- Budgeting For Staff Compensation

- Benefits, Taxes, And Legal Considerations

- Negotiation And Pay Review Playbook

- Benchmarking Tools And Data Sources

- Common Mistakes Churches Make

- FAQs

What Pastor Compensation Includes

Base Salary Versus Total Compensation

Base salary is the straightforward cash paycheck a pastor receives. Total compensation is everything else that adds value, like housing, insurance, retirement contributions, paid time off, car allowances, and professional development. When comparing offers or building a budget, look at total compensation, not just the line labeled salary. A lower base plus a generous housing allowance or full benefits can be worth more than a higher base with no benefits.

Common Noncash Benefits

Many churches supplement cash pay with benefits that reduce a pastor’s out-of-pocket expenses. Typical noncash items include:

- Employer‑paid health, dental, and life insurance

- Housing allowance or church‑owned parsonage

- Utilities, internet, or phone reimbursement

- Vehicle or mileage allowance, or church vehicle use

- Paid sabbatical, vacation, and continuing education funds

- Conference travel and ministry resources

- Tuition assistance or student loan help

These benefits affect family finances and tax treatment, so document them clearly in the call or employment letter.

Housing Allowance And Parsonage Options

Housing allowance is a designated portion of compensation set by the church, excluded from federal income tax up to the amount used to house the pastor, but it must be formally designated. A parsonage is church‑provided housing, with utilities and maintenance often covered. Each option changes how expenses and taxes are reported, so churches should:

- Vote the housing allowance in official minutes

- Provide an annual written designation

- Encourage pastors to keep records of actual housing expenses

Proper documentation protects both the church and the pastor at tax time.

Retirement, Insurance, And Payroll Taxes

Retirement plans vary, from denominational pensions to 403b or SEP IRA accounts. Employer contributions, vesting schedules, and eligibility matter when comparing packages. Insurance items commonly included are health, dental, disability, and life insurance. On payroll taxes, clergy have a unique situation: housing allowance is generally excluded from income tax but not always from self‑employment taxes, and ministers may need to file for or against Social Security exemption under Form 4361. Churches must also decide how to handle withholding, unemployment coverage, and worker’s comp. These areas are technical, so a tax adviser and clear payroll policies are essential.

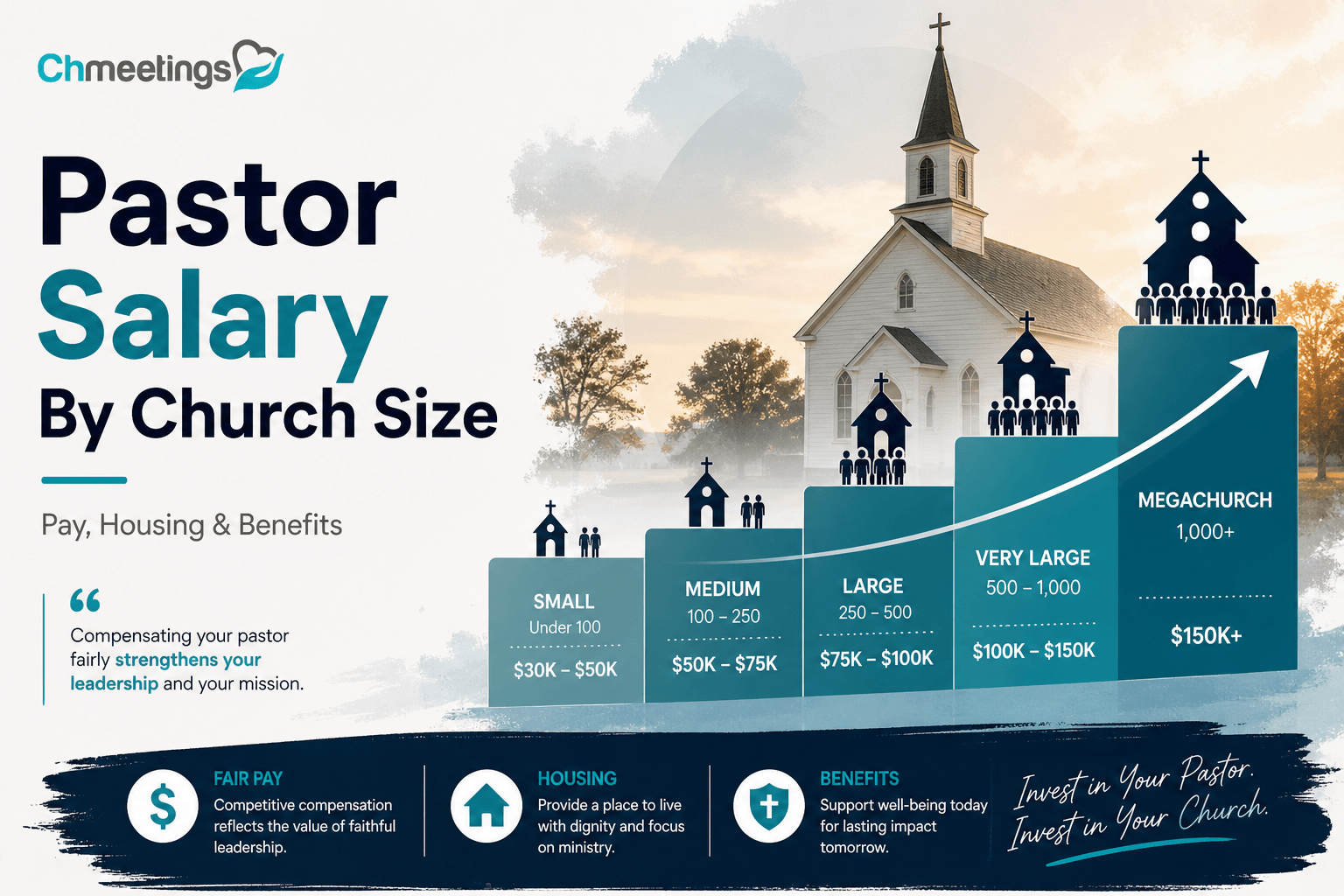

Comparing Salaries By Church Size

Under 50 Members

Most churches under 50 operate with very tight budgets. Pastoral roles are commonly volunteer or stipend based, often bivocational. Expect minimal or no employer benefits. Compensation frequently includes mileage, occasional housing help, or small monthly stipends. Skillful time management and outside income are common realities.

50 To 150 Members

At this size, churches often move toward a consistent, possibly part‑time paid pastor, or a full‑time pastor with modest pay. Benefits may be limited, but churches start budgeting for health insurance, retirement contributions, and professional development. One person often carries preaching, administration, and pastoral care duties.

150 To 300 Members

Churches in this range typically can support a full‑time senior pastor and sometimes one or two staff roles. Compensation becomes steadier, with clearer benefit packages, housing allowance or parsonage options, and modest employer retirement contributions. Expect more formalized job descriptions and periodic reviews.

300 To 500 Members

When attendance reaches this level, staffing expands and salaries become more competitive. Churches often provide comprehensive benefits, larger housing allowances, and defined retirement plans. Role specialization increases, and compensation committees or boards usually follow formal salary bands.

500 To 1,000 Members

This size supports multiple full‑time staff and specialists. Senior pastors’ packages are more sophisticated, with larger housing allowances or parsonage benefits, stronger retirement funding, and possible performance incentives. Churches may employ HR processes for salary benchmarking and written compensation policies.

Over 1,000 Members

Large or multi‑site churches have the budgets to offer market competitive salaries and full benefits packages, often with bonuses, equity‑style incentives for multi‑site leaders, and professional HR and finance teams overseeing compensation. Compensation tends to be benchmarked against denominational and regional data and managed through formal committees and policies.

Role-Based Pay Differences

Senior Pastor Pay Patterns

Senior pastors carry the broadest responsibility, so they usually receive the highest compensation in the staff. Pay reflects preaching load, administrative oversight, staff management, fundraising, and public representation. Packages often include housing support, retirement contributions, paid sabbaticals, and performance reviews tied to strategic goals.

Associate Pastor And Staff Pastors

Associate and staff pastors are paid based on portfolio, experience, and educational level. They earn less than the senior pastor, but ministry specialty and program leadership can raise pay. Larger churches often have step scales or salary bands to ensure internal equity and clarity for promotion.

Youth, Children, And Worship Leaders

These roles vary widely. Many youth and children’s pastors start part‑time and move to full‑time as programs grow. Worship leaders who bring high production skills or lead multiple services may command higher pay. Compensation often reflects skills, volunteer management responsibilities, and technical demands.

Part-Time And BiVocational Roles

Part‑time and bivocational pastors are common in smaller congregations. Pay is usually hourly or stipend based, with few benefits. Churches should set clear expectations about availability and responsibilities, and consider modest benefits or professional development support to reduce burnout and turnover.

Regional And Denominational Trends

Cost Of Living Adjustments

Geography changes what a given salary actually buys. Urban pastors face higher housing and living expenses, so churches often apply cost of living adjustments or regional multipliers when setting pay. Regular reviews using local indices help keep compensation fair and sustainable.

Denomination Salary Guidelines

Many denominations publish salary tables and benefits recommendations. Those guidelines are useful benchmarks for fairness and accountability, especially for smaller churches that lack HR resources. Using denominational guidance builds trust and helps with recruiting.

Urban Versus Rural Comparisons

Urban churches generally pay more in cash compensation to offset higher living costs, while rural churches may offer lower cash pay but more housing support or lower living expenses. Expectations for staff specialization also differ, with rural pastors often wearing more hats.

State And Federal Reporting Requirements

Churches must comply with payroll and tax reporting rules. Common obligations include issuing W‑2s to employed staff, filing Form 941 quarterly for payroll taxes, and handling unemployment and worker’s comp where required. Clergy tax issues are unique, so keep records for housing allowance designation and advise pastors about Form 4361 if they consider Social Security exemption. When independent contractors are used, issue 1099‑NEC appropriately. Clear, compliant payroll practices reduce legal risk and build trust with staff.

Note: tracking compensation, benefits, and payroll records in a church management app can simplify reporting and keep your finance team organized while you focus on ministry.

Factors That Drive Pay Levels

Church Budget And Revenue Mix

A pastor’s pay follows the money a church actually has, not an ideal number. Tithes, recurring donations, event revenue, and facility income create the pool available for salaries. One large gift can temporarily inflate capacity, so focus on sustainable, recurring revenue when setting pay. Distinguish unrestricted operating funds from designated or capital gifts, because budgets funded by one-time gifts shouldn’t create permanent pay obligations.

Experience, Education, And Credentials

Years in ministry, seminary or vocational degrees, ordination status, and denominational expectations shape market value. A pastor with specialized skills, like counseling or development, will command more than a generalist. Churches should document minimum and preferred qualifications in the job description so expectations and pay line up.

Scope Of Responsibilities And Hours

Pay reflects what you’re asking someone to do and how much time they invest. Preaching only, preaching plus administration, or preaching plus multi-campus oversight all carry different price tags. Be explicit about expected hours, on-call frequency, travel, and supervisory duties. Two part-time roles that together equal full-time deserve compensation comparable to a single full-time position.

Congregational Expectations And Growth

Growth plans and congregational culture affect compensation. A small rural church may value long tenure and local fit over market pay. A growing, mission-driven church with ambitious outreach goals will need competitive packages to recruit leaders who can scale ministry. Align compensation with the congregation’s stated priorities so pay supports, rather than distracts from, your vision.

How To Calculate A Fair Salary

Salary Per Member Formula

Salary per member is a simple starting point, calculated as salary equals dollars per active member times number of active members. Choose your per-member rate based on size, location, and budget health. Smaller churches often use a higher per-member figure to reflect fewer economies of scale. Use this method for quick benchmarking, not as the only determinant.

Example formula:

salary = per_member_rate × active_members

Suggested per_member_rate ranges, illustrative:

- Small churches under 150, $200 to $600 per member

- Mid churches 150 to 500, $150 to $450 per member

- Larger churches, $100 to $300 per member

Adjust for local cost of living and benefit packages.

Percent Of Budget Method

This method ties compensation to what the church can sustainably afford. Decide what share of the annual operating budget goes to the senior pastor’s total compensation, including benefits.

Common guidance:

- Under 150 members, senior pastor 25% to 40% of budget

- 150 to 500 members, 15% to 25% of budget

- Over 500 members, 10% to 18% of budget

Use the lower end if multiple staff need support, and the upper end if the senior pastor is the primary paid leader. Always treat benefits and housing as part of the total percent.

Staff-To-Member Ratio Approach

First, decide how many full-time staff you need to fulfill ministry goals, then allocate an overall personnel budget and divide it across roles. This method is useful when planning growth or restructuring.

Simple steps:

- Set desired staff-to-member ratio, for example one full-time staff per 80 to 150 attendees depending on program complexity.

- Multiply FTEs by market salary benchmarks for each role.

- Confirm the total fits your budget percent targets and adjust roles or pay bands if needed.

This approach links capacity to mission, not just to a single salary line.

Pastor Salary Calculator Inputs

A reliable calculator needs these inputs to produce a defensible number:

- Active member count and average weekly attendance

- Annual operating budget and unrestricted giving

- Local cost of living or regional multiplier

- Housing arrangement, housing allowance amount or parsonage value

- Full-time equivalent of the role, expected hours

- Benefits offered, employer retirement, health insurance costs

- Experience, education, and any specialty pay (counseling, multi-site)

- Denominational recommendations or regional benchmarks

A church management app like ChMeetings can supply attendance and giving reports quickly, removing guesswork and speeding realistic calculations.

Examples For 50, 100, 300, 500 Members

These illustrations use three methods, with a sample budget assumption of $1,200 annual giving per active member to create an operating budget. Numbers are total compensation estimates, including benefits.

Assumption: operating budget = members × $1,200

1) 50 members, budget $60,000

- Per member method, $300 × 50 = $15,000

- Percent of budget, 30% × $60,000 = $18,000

- Staff ratio method, one 0.5 FTE pastor at market equivalent = $20,000 total comp

Takeaway, realistic pastor total comp likely $15k to $25k, often supplemented by housing or stipend.

2) 100 members, budget $120,000

- Per member, $350 × 100 = $35,000

- Percent of budget, 30% × $120,000 = $36,000

- Staff ratio, one 0.75–1.0 FTE pastor = $30,000 to $50,000

Takeaway, expect roughly $30k to $45k total comp depending on benefits and hours.

3) 300 members, budget $360,000

- Per member, $250 × 300 = $75,000

- Percent of budget, 20% × $360,000 = $72,000

- Staff ratio, senior pastor plus several staff, senior pastor market = $65,000 to $95,000

Takeaway, mid to upper range reflects full-time role, housing allowance, and benefits.

4) 500 members, budget $600,000

- Per member, $200 × 500 = $100,000

- Percent of budget, 15% × $600,000 = $90,000

- Staff ratio, senior pastor with expanded leadership responsibilities = $90,000 to $140,000

Takeaway, compensation rises but becomes a smaller portion of a larger budget, and benefits packages become more comprehensive.

These are examples, not prescriptions. Local cost of living, denominational guidance, and expected role scope change the numbers.

Building A Formal Compensation Policy

Salary Banding And Job Descriptions

Create clear salary bands for each role tied to experience and education. Pair each band with a precise job description listing responsibilities, time expectations, supervision structure, and measurable outcomes. Bands prevent ad hoc decisions and help with recruitment, internal equity, and transparent conversations when roles change.

Pay Review Cadence And Criteria

Set an annual pay review for each staff member and a market benchmark review every two to three years. Use consistent criteria, including tenure, performance, market shifts, and budget health. Define who reviews pay, how conflicts of interest are managed, and how increases are approved and documented.

Performance Metrics Linked To Pay

Link a portion of compensation to agreed objectives, while keeping a solid base salary. Use a mix of quantitative and qualitative measures:

- Quantitative: attendance growth, small group participation, volunteer retention, giving trends tied to stewardship goals

- Qualitative: pastoral care quality, leadership development, staff collaboration, alignment with church vision

Document expectations up front, review outcomes annually, and separate mission goals from administrative tasks.

Checklist: Compensation Policy Essentials

- Written job descriptions for every paid role

- Salary bands with minimum and maximums

- Annual review schedule and market benchmarking timeline

- Documented benefits and housing allowance practices

- Payroll procedures, tax compliance, and housing designation minutes

- Severance, sabbatical, and transition policies

- Conflict of interest and confidentiality rules for compensation decisions

- Communication plan for staff and congregation about policy changes

A written policy protects both staff and the church, and makes future transitions smoother.

Budgeting For Staff Compensation

Recommended Budget Percentages

Use benchmarks but adapt to mission and size. Rough guidance:

- Under 150 members, staff compensation 40% to 60% of budget

- 150 to 500 members, 30% to 45% of budget

- Over 500 members, 25% to 35% of budget

Within that, senior pastor total comp often occupies 10% to 30% of the personnel budget, depending on staff size and role scope.

Forecasting Raises And Benefits Costs

Build annual raise estimates into the budget, typically 3% to 5% as a baseline, more if inflation is high. Model employer benefit cost increases separately, since health and retirement costs can rise faster than salaries. Run at least three year scenarios, showing best case, expected, and conservative outcomes.

Emergency Reserves And Transition Funds

Maintain a payroll reserve equal to 3 to 6 months of total payroll to cover unexpected shortfalls or revenue dips. In addition, keep a pastoral transition fund equal to 3 to 9 months of the senior pastor’s total compensation to allow for healthy transitions and search processes. These funds protect ministry continuity and reduce rushed decisions.

Aligning Compensation With Strategic Goals

Make compensation decisions mission driven. If the strategic plan prioritizes outreach or youth ministry, allocate budget to roles that achieve those goals. Use data from your backend, attendance and giving trends, and volunteer capacity to justify investments. A church management app can provide the reports you need to link compensation choices to measurable ministry outcomes, so funding follows strategy, not tradition.

Benefits, Taxes, And Legal Considerations

Structuring A Housing Allowance Correctly

Housing allowance must be a formal line item, not an oral promise. Best practice steps:

- Have the church board vote the allowance and record the vote in minutes before payments start.

- Put a written designation in the pastor’s contract that states the annual amount and the method for annual re‑designation.

- Keep pastor receipts and records of actual housing expenses, because the exclusion is limited to the amount used for housing, not simply the designated amount.

- If the church provides a parsonage, estimate the fair rental value and record that as part of total compensation.

- Review the designation annually after any salary change or major housing expense shift.

Consult a tax adviser for edge cases, like dual housing situations or significant renovations, so the church and pastor avoid unexpected tax exposure.

Payroll Taxes And Withholding Practices

Clergy tax rules are unusual, so clarity matters. Key items to cover:

- Classify workers consistently. Paid staff typically receive W‑2s; true independent contractors get 1099‑NEC when rules apply. Misclassification creates IRS and state risk.

- Ministers are subject to self‑employment tax rules for Social Security unless they successfully apply for an exemption using Form 4361. Income tax withholding is optional, but if the pastor requests withholding, set it up and file W‑2s.

- File required employer tax returns and deposits on time, including Form 941 quarterly filings and federal and state unemployment returns where applicable. States vary on clergy unemployment coverage and worker’s compensation requirements, so check local law.

- Use a reliable payroll provider or payroll service inside your church management process to automate deposits, filings, and year‑end forms. Accurate payroll reduces audit risk and frees leaders to lead.

Benefits Packages Churches Should Offer

Benefits are a major part of total compensation and a recruiting tool. Consider tiering packages by church size and role:

- Essentials: employer retirement contribution or match, health insurance contribution or stipend, paid time off, and a housing allowance or parsonage.

- Strong packages: group life and disability insurance, employer‑paid retirement (403b, SEP, or denominational pension), paid continuing education, and paid sabbatical policy.

- Size‑appropriate additions: family coverage, dependent care or childcare stipends, tuition assistance, and commuter or vehicle allowances. Design eligibility rules, waiting periods, and employer cost‑share levels clearly. When budget is tight, be explicit whether the church provides cash stipends in lieu of group plans, and document tax treatment. Communicate the full value of benefits during hiring, not just base pay.

Avoiding Common Compliance Pitfalls

Compliance failures are almost always avoidable with simple systems. Look out for:

- No written housing designation or missing board minutes. That’s an easy audit trigger.

- Misclassifying clergy or staff and failing to issue the correct tax forms.

- Ignoring state requirements for unemployment or worker’s compensation coverage.

- Poor record keeping for benefits eligibility, contributions, and personnel actions. Prevent problems by using checked workflows for hiring and payroll, keeping minutes and contracts in one secure place, and conducting an annual compliance review with a CPA or attorney familiar with church law.

Negotiation And Pay Review Playbook

Preparing For A Compensation Conversation

Preparation makes these talks constructive. Before the meeting:

- Pull together total compensation data, not just base salary. Show housing, benefits, and employer costs.

- Bring role description, recent performance notes, and church budget projections.

- Benchmark the proposed package against denominational guidance and local market data.

- Decide in advance who speaks for the church, what approvals are needed, and how decisions will be communicated to staff and congregation. Start the conversation with mutual goals: what the church needs and what will help the pastor thrive.

Setting Objective Evaluation Criteria

Subjective praise feels good, but pay needs measurable anchors:

- Define a small set of objective metrics tied to the role, like attendance growth, small group engagement, volunteer retention, stewardship outcomes, and completion of leadership development goals.

- Combine those with qualitative measures, for example peer and congregational feedback, conflict management, and spiritual leadership.

- Use a simple rubric with clear rating bands and document outcomes before discussing pay. Make review dates predictable and stick to them, so compensation follows performance, not preference.

Offering Creative Noncash Compensation

When cash is limited, get creative inside legal boundaries:

- Additional paid time off, a defined sabbatical cadence, or a flexible schedule.

- Student loan assistance, tuition reimbursement, or paid continuing education.

- Housing upgrades, moving support, or a car allowance.

- Professional development funding, conference travel, and ministry resource stipends. Value noncash items transparently, explain tax treatment, and document them in the employment agreement so there are no surprises later.

Handling Retention And Exit Situations

Plan for both staying and leaving:

- Retention starts with regular career conversations, role development, and small, timely recognition. Address workload and burnout risks early.

- For exits, have a written severance and transition policy that covers notice periods, final pay, benefits continuation, and pastoral handoff.

- Conduct exit interviews to learn what worked and what did not. Use those insights to adjust job design, compensation, or support systems. Treat transitions as ministry moments, not just HR events, and keep communications clear to protect both the person and the congregation.

Benchmarking Tools And Data Sources

National Surveys And Denominational Data

Start with published datasets:

- Denominational salary guides, pension boards, and conference offices often publish role‑specific ranges and benefits recommendations tailored to their polity.

- National sources like the Bureau of Labor Statistics provide occupational pay data for clergy that can establish a floor or ceiling. Crosscheck multiple sources so you do not rely on a single snapshot.

Church Compensation Calculators

Good calculators force you to include total compensation inputs:

- Use tools that accept attendance, operating budget, housing arrangement, benefits costs, and regional cost‑of‑living multipliers.

- Feed the calculator accurate data from your giving and attendance reports so outputs reflect reality. A well‑constructed calculator helps frame realistic offers and makes conversations less subjective.

Peer Benchmarking And Regional Networks

There is no substitute for local context:

- Compare with nearby churches of similar size and demographic profile. Regional costs and expectations can differ dramatically from national averages.

- Join denominational networks, clergy cohorts, or area pastoral groups that share anonymized salary ranges. Peer benchmarking helps confirm whether a number is competitive where you actually recruit.

When To Hire A Compensation Consultant

Bring external help when complexity or risk is high:

- Hire a consultant for multi‑site leadership packages, major staff restructures, contested negotiations, or when legal exposure is significant.

- A consultant can create salary bands, assess total rewards competitiveness, and advise on local tax and benefit implications. Weigh consultant fees against the cost of a poor hire or legal exposure, and ask for references from other churches.

Common Mistakes Churches Make

Underestimating Total Cost Of Hire

Salary is only part of the bill. Calculate true cost by adding:

- Employer payroll taxes and benefit contributions, onboarding and training, technology and office overhead, and recruitment expenses. A simple formula to start with: total cost = base pay + employer taxes + benefits + overhead + one‑time recruitment costs. Use that number when forecasting and building reserves.

Ignoring Benefits And Tax Implications

Treat benefits and taxes as strategic, not optional:

- Overlooking retirement, health, or housing tax implications can create unexpected liabilities for pastors and the church.

- Small churches sometimes assume benefits are optional, then face turnover when pastors find better total packages elsewhere. Budget benefits intentionally and document tax treatments to avoid surprises.

Relying On Anecdotes Instead Of Data

Stories are useful, but not enough:

- Avoid setting pay based solely on what another church “did last year” or a well‑meaning opinion. Use data from surveys, calculators, and local peers.

- Collect internal metrics from your member and giving reports to justify sustainable salaries tied to real capacity. Data reduces resentment and improves transparency.

Skipping Written Policies And Reviews

Verbal promises lead to problems:

- Not having written compensation policies, review cadences, or documented housing designations creates legal and relational risk.

- Annual written reviews, documented raises, and a stewardship of minutes preserve institutional memory and protect both staff and congregation. Invest time in clear, living policies. They make future decisions easier and fairer.

FAQs

What Is The Average Salary For A 100-Member Church?

Expect a full picture, not just base pay. For a 100-member church, the realistic total compensation range for a senior pastor is roughly $30,000 to $45,000 per year, including housing allowance or parsonage value and common benefits. Smaller budgets, part-time roles, or limited benefits push toward the lower end; churches in higher cost areas or offering full benefits sit at the top. Use total compensation when comparing offers.

What Is The Average Salary For A 300-Member Church?

For a 300-member congregation, senior pastor total compensation typically falls in the $65,000 to $95,000 range. That reflects a full-time role with housing support, retirement contributions, and basic health benefits. Local cost of living, denomination guidelines, and whether the pastor oversees multiple staff or sites will shift the number.

How Much Does A Senior Pastor Earn By Church Size?

Typical total compensation ranges, including housing and common benefits:

- Under 50 members, often volunteer or stipend roles, $0 to $25,000.

- 50 to 150 members, part-time to modest full-time pay, $15,000 to $45,000.

- 150 to 300 members, stable full-time roles, $45,000 to $85,000.

- 300 to 500 members, more competitive packages, $65,000 to $120,000.

- 500 to 1,000 members, senior pastor packages with fuller benefits, $90,000 to $160,000.

- Over 1,000 members, market competitive and often custom packages, $120,000 and up.

These are ranges, not prescriptions. Adjust for regional cost, denominational guidance, and role scope.

What Should A 50-Member Church Budget For Pay?

A realistic total compensation target for a 50-member church is usually $15,000 to $25,000 annually, often a part-time stipend or a 0.5 FTE arrangement. If the church offers housing support or a parsonage, that reduces cash needs. When cash is tight, document expectations clearly, consider a modest benefits stipend, and plan for payroll reserves so the arrangement is sustainable.

How Do Youth Pastor Salaries Vary By Size?

Youth pastor pay tracks program scale and hours:

- Small churches under 150 members, often part-time or stipend work, roughly $5,000 to $20,000.

- Mid churches 150 to 300 members, part-time to full-time roles, $20,000 to $45,000.

- Larger churches 300 to 500 members, full-time with benefits, $35,000 to $60,000.

- 500+ members, experienced youth directors or multi-site youth leads, $45,000 to $80,000+.

Special skills, grant funding, or fundraising responsibilities can raise these numbers. Always state FTE expectations and benefits in the job description.

How Do I Use A Pastor Salary Calculator?

Use a calculator to get a defensible starting point, not the final answer:

- Gather accurate inputs: active member count, average weekly attendance, annual operating budget, current unrestricted giving, regional cost multiplier, housing arrangement, expected FTE, and benefits costs.

- Choose a method to weight results, for example per-member, percent of budget, or staff-to-member ratio. Run all three and compare.

- Add employer costs, payroll taxes, and reserves to the output so you see the true budget impact.

- Document assumptions and produce a total compensation figure, including housing and benefits.

- Review with leadership, benchmark against local peers or denominational tables, and adjust for ministry goals.

A church management app that houses attendance and giving reports will speed step one and keep your inputs reliable, which makes the calculator output far more useful.

What Percentage Of Budget Should Go To Staff?

Use these common benchmarks as a starting point:

- Under 150 members, personnel 40% to 60% of the operating budget.

- 150 to 500 members, personnel 30% to 45% of the operating budget.

- Over 500 members, personnel 25% to 35% of the operating budget.

Within the personnel budget, the senior pastor often accounts for roughly 10% to 30% depending on staff size and role scope. Build in payroll reserves equal to 3 to 6 months of payroll, plus a pastoral transition fund, and align staffing percentages with strategic priorities so compensation supports mission.