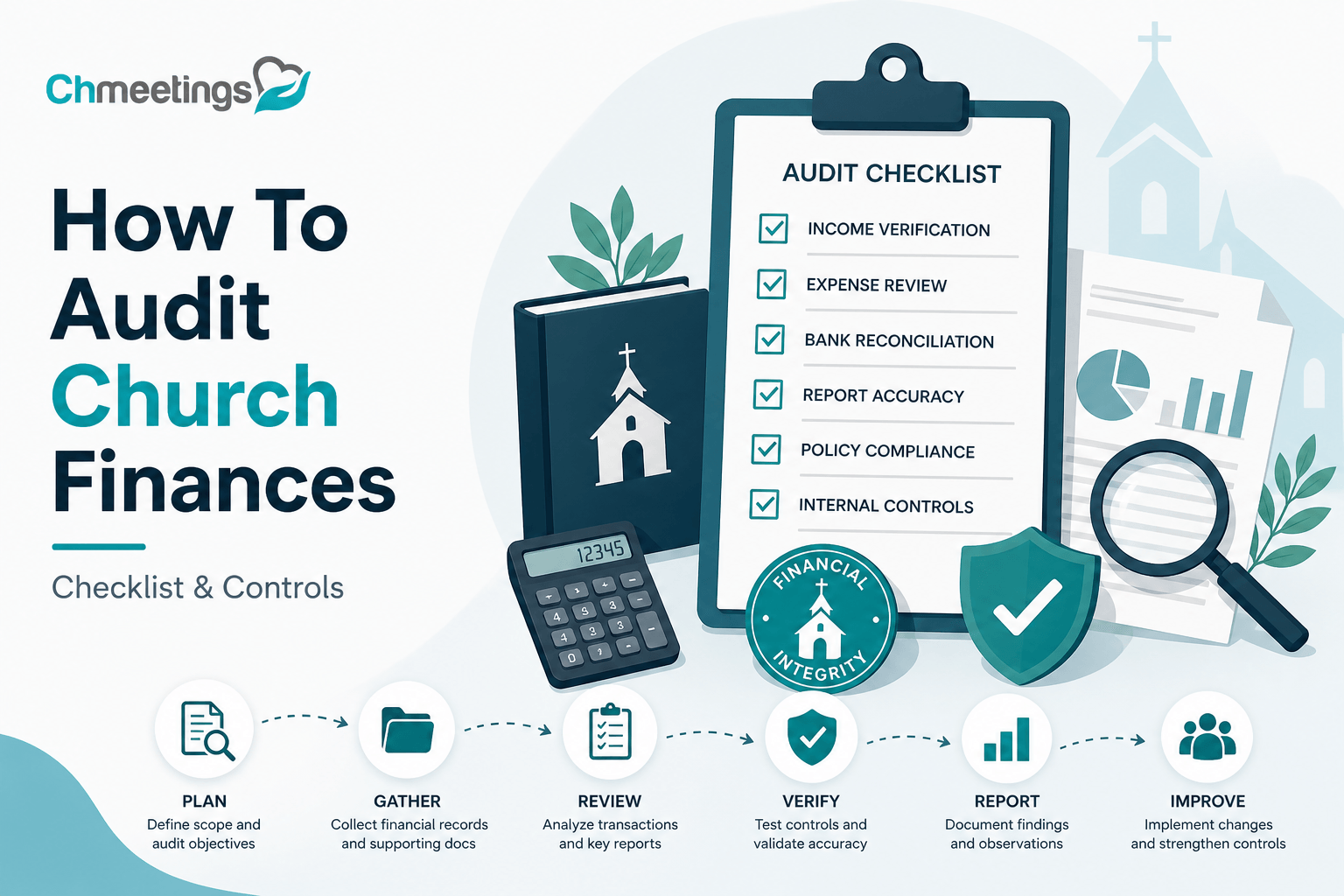

- What Is A Church Audit?

- Preparing Your Church For An Audit

- Choosing The Right Audit Type

- Selecting An Auditor Or Firm

- Building Internal Controls That Work

- Step-By-Step Financial Audit Process

- Auditing Giving And Donations

- Auditing Payroll, Benefits, And Taxes

- Auditing Facilities And Fixed Assets

- Reporting Findings And Action Plans

- Templates, Checklists, And Samples

- Common Pitfalls And Red Flags

- Tracking Key Metrics After Audit

- FAQs

What Is A Church Audit?

Definition And Purpose

A church audit is an independent review of the congregation’s financial records and controls, designed to confirm accuracy, completeness, and stewardship of funds. It looks at financial statements, transactions, policies, and internal controls to identify errors, omissions, or risks. The goal is accountability to the congregation and donors, protection for leadership, and practical recommendations to strengthen finance processes.

Types Of Assurance Reports

Auditors issue different kinds of reports depending on the work done. A full audit results in an opinion, which can be unqualified, qualified, adverse, or a disclaimer. A review gives limited assurance, and a compilation simply assembles statements without opinion. Agreed-upon procedures produce a factual findings report tied to specific tests. Know what level of assurance you need before hiring.

Legal, Tax, And Denominational Triggers

Audits can be required by law, funders, or denominational rules. Examples include state charity registration thresholds, grant or government funding stipulations, and denominational governance requiring annual reviews. Other triggers are leadership transitions, allegations of mismanagement, or sudden financial irregularities. Check your bylaws, grant agreements, and state nonprofit rules to see if an audit is mandatory.

Preparing Your Church For An Audit

Gather Key Financial Documents

Create a complete, organized packet of documents for the auditor: general ledger, trial balance, bank statements and reconciliations, contribution records and donor statements, payroll files and tax filings, expense receipts, vendor contracts, insurance policies, budgets and minutes from finance meetings, and a fixed asset schedule. Digital copies speed the process, and exporting reports from your church management software makes compiling giving and member data easier.

Assign Roles And Responsibilities

Name a single point person for the audit, usually the finance director or treasurer, plus a backup. Define who will gather documents, who will answer auditor questions, and who has authority to approve adjustments. Involve a finance committee liaison and the senior pastor for governance matters. Clear roles reduce delays and confusion.

Clean Up Records Before Fieldwork

Reconcile bank accounts, clear stale checks and unapplied donations, correct misclassified entries, and document restricted fund balances. Update payroll and vendor records, and prepare explanations for any large or unusual transactions. Tidying these items ahead of time lowers auditor hours and produces a smoother fieldwork phase. If you use a church management app, export current giving and member reports to avoid manual rekeying.

Create A Timeline And Communication Plan

Set target dates for document delivery, entrance and exit meetings, and draft report review. Tell staff and volunteers who will be contacted and how questions will be handled. Prepare a short message for the congregation explaining the audit purpose, timing, and who will answer inquiries. Routine updates to the finance committee keep governance informed and build trust.

Choosing The Right Audit Type

Internal Review Versus External Audit

An internal review, done by staff or a committee, helps check controls and spot problems at lower cost, but it lacks independence. An external audit, performed by a licensed CPA firm, provides the highest level of assurance and is often required by funders or law. Choose external for grants, significant public accountability, or when independence is essential.

Agreed-Upon Procedures And Reviews

Agreed-upon procedures let you specify tests, such as cash handling or payroll, and receive a factual report of findings. Reviews are broader but provide limited assurance, focusing on analytical procedures and inquiries. Both options cost less than a full audit and work well for targeted concerns or interim checks between full audits.

Peer Review And Denominational Options

Some denominations or networks offer peer review programs or standardized reviews tailored to churches. These can be less expensive and preserve denominational consistency in reporting. Peer reviewers often bring relevant ministry context, but check their independence and technical depth before relying on the result for external compliance.

Scope And Cost Tradeoffs

Scope drives cost. A full audit covers financial statements and internal controls, so it takes more time and fees. Narrower engagements, like agreed-upon procedures, target specific risks at lower cost. Prioritize areas that pose the greatest risk, such as cash receipts, restricted giving, and payroll, and consider a rotating schedule of full audits and targeted reviews to balance assurance and budget.

Selecting An Auditor Or Firm

Qualifications To Require

Require a licensed CPA or firm with nonprofit and church experience, familiarity with fund accounting and donor restriction rules, professional liability insurance, and proof of independence. Experience with payroll, multi-site operations, or grant compliance is a plus. Ask that they follow professional auditing standards.

Interview Questions To Ask

Ask how many churches they serve and their experience with organizations your size. Who will perform the fieldwork, and will a partner or manager be involved? What procedures are standard in their church audits? How do they detect fraud risk, what is the expected timeline, and how are fees billed? Ask for examples of practical recommendations they’ve made to other churches.

Checking References And Samples

Request client references, especially other congregations, and review sample reports to assess clarity and usefulness. Call references and ask about responsiveness, professionalism, and whether the auditor offered actionable guidance. Verify the firm’s standing with state boards and any disciplinary history.

Engagement Letter Essentials

Before work starts, get a signed engagement letter that spells out the scope of services, responsibilities of management, timelines, fee estimates and billing terms, deliverables and report format, confidentiality terms, and limitations of liability. The letter protects both the church and the auditor and frames expectations for a smooth engagement.

Building Internal Controls That Work

Segregation Of Duties Practices

Segregation of duties reduces opportunity for error or misuse by splitting key tasks between people. Separate cash handling from recording, reconcile bank statements by someone who does not prepare deposits, and have a different person approve vendor payments. Small churches often can’t fully segregate, so use compensating controls instead, like rotating duties, mandatory dual signatures, and regular finance committee spot checks. Keep simple job descriptions that spell out who does what, and keep oversight documented.

Offering And Cash Handling Controls

Count offerings with at least two unrelated counters in a secure room, use sequentially numbered deposit slips, and put cash into tamper-evident bags immediately. Record totals on a count sheet, reconcile to the bank deposit, and store funds in a locked safe between counting and deposit. Train counters on handling loose checks and cash, require receipts for all cash disbursements, and log any discrepancies with signatures from counters and a supervisor.

Approval, Reconciliation, And Access Rules

Set clear approval thresholds for purchases and reimbursements, require back-up documentation for every payment, and enforce pre-authorized budget limits. Reconcile bank accounts, credit cards, and petty cash monthly, and have a trustee or finance committee member review reconciliations and bank statements. Apply the principle of least privilege for physical keys and digital accounts, and keep an up-to-date vendor master list that only authorized staff can change.

IT And eGiving Security Basics

Protect online giving and accounting data with strong passwords, two-factor authentication, regular software updates, and routine backups. Verify your eGiving vendor is PCI compliant, review access logs, and limit admin rights to a few trusted people. Export and reconcile online giving reports to bank deposits each period. If you use church management software like ChMeetings, enable role-based permissions and audit logs to track edits and exports.

Step-By-Step Financial Audit Process

Risk Assessment And Planning

Start by identifying high-risk areas, such as cash receipts, payroll, and restricted funds, then set materiality and scope. Review prior audit findings, meeting minutes, and any unusual transactions from the year. Build a timeline with milestones for document requests, fieldwork, and draft report review. Communicate expectations to staff and volunteers so gathering documents won’t bog down ministry work.

Sampling And Testing Procedures

Choose sampling methods that match the risk, use random sampling for broad testing, and apply judgmental sampling for high-risk items. Test offering deposits, large or unusual expenses, payroll changes, and vendor payments for proper authorization and support. Use cut-off testing around year-end to confirm transactions are recorded in the correct period. Document selections and exceptions so results can be reproduced.

Fieldwork Tasks And Checklists

Fieldwork is hands-on, not theoretical. Confirm bank balances and reconciliations, vouch a sample of deposits to deposit slips and bank statements, inspect payroll files and tax filings, and verify restricted fund activity against donor intent. Observe an offering count if possible, test access controls, and review minutes for approvals. Use a checklist to track each evidence item, note who provided it, and mark items cleared or outstanding.

Final Review And Sign-Off

Compile audit findings, classify them by severity, and prepare a management letter with recommended fixes and timelines. Discuss draft findings with the finance director and senior pastor, resolve factual issues, and document agreed corrective actions. Present the final report to the finance committee or board, obtain signatures on any adjustments, and schedule a follow-up review to confirm remediation.

Auditing Giving And Donations

Counting And Recording Offerings

Verify the offering count process is consistently followed, compare count sheets to deposit slips, and trace deposits to the bank. Ensure checks are endorsed promptly and recorded with donor names where appropriate. Confirm the general ledger or giving module reflects the deposits accurately, and investigate any timing differences or unexplained variances.

Reconciling eGiving Platforms

Reconcile eGiving provider reports to bank deposits routinely, match gross receipts, fees, and refunds, and reconcile net deposits to the ledger. Allocate processor fees to expense accounts or donor-designated funds according to policy. Export giving reports from your church management software to speed matching and identify donors whose gifts didn’t transmit or were refunded.

Tracking Restricted And Designated Gifts

Tag restricted gifts on receipt and segregate them in the ledger so donor intent is always visible. Reconcile restricted fund balances monthly, and require board approval to move funds or use them for other purposes. Keep documentation showing how restricted gifts were spent, so donors and auditors can trace dollars from gift to program.

Donor Statements And Acknowledgments

Ensure year-end donor statements reflect the date of gift and the correct amount, and send timely acknowledgments that meet IRS requirements for deductible gifts. Have a process to correct statement errors and reissue documents when needed. Use your church management software to generate statements consistently, reducing manual errors and saving time.

Auditing Payroll, Benefits, And Taxes

Payroll Processing Controls

Review payroll setup for authorized pay rates, signed hire forms, and timekeeping controls. Require an approver who is separate from the payroll preparer, reconcile payroll registers to bank payments, and review payroll liability accounts each month. If a third-party payroll service is used, confirm their controls and obtain reports that show changes to employee data.

Pastoral Compensation And Housing Allowance

Document pastoral compensation decisions in board minutes and specify housing allowance amounts annually. Keep a formal record designating the housing allowance, including calculations and dates, so it’s clear for tax purposes. Verify payroll records and W-2s reflect compensation and any housing reporting correctly.

Independent Contractors And 1099s

Gather W-9s for contractors, classify workers consistently, and document the justification when someone is treated as an independent contractor. Issue 1099-NEC forms for reportable payments over the threshold and reconcile contractor payments to 1099s before filing. Misclassification risks payroll tax exposure, so maintain clear contracts and task descriptions.

Tax Filings And Withholding Checks

Confirm payroll tax deposits are timely and reconciled to payroll tax returns, validate quarterly 941 filings and annual W-2s, and check state unemployment filings where applicable. Reconcile payroll tax liabilities each month and clear any discrepancies promptly. Keep records of deposit schedules, confirmations, and correspondence with tax authorities to avoid penalties.

Auditing Facilities And Fixed Assets

Maintaining An Asset Register

Create a single, current asset register that lists every building, parcel, furniture item, vehicle, and major piece of equipment. For each item include acquisition date, cost, location, serial or VIN numbers, donor or funding source, and any restriction on use. Update the register whenever an asset is added, moved, sold, or disposed of, and require two signatures for removals. A reliable register makes year-end reconciliations faster and prevents unnoticed losses during leadership transitions.

Depreciation And Capitalization Rules

Set clear capitalization thresholds so smaller purchases are expensed and only material items are capitalized and depreciated. Use consistent depreciation methods and useful lives that match your denomination’s practice or accounting guidance for nonprofits. Document policy in writing and apply it consistently during audits, so auditors can verify calculation and support. Review large repairs versus capital improvements, because misclassification can distort both asset balances and operating results.

Facility Use Income And Custodial Funds

Track facility rental income separately from donations, with written agreements showing rates, insurance requirements, and damage deposits. Treat third-party collections held temporarily, such as event ticket sales or outside group deposits, as custodial funds and never record them as church revenue. Reconcile facility use receipts to contracts and bank deposits monthly, and issue statements or refunds promptly when contracts end. Clear policies prevent misunderstandings and protect donor trust.

Physical Inventory And Insurance Checks

Do a physical walk-through at least annually and reconcile the results to the asset register and insurance schedule. Note missing, damaged, or obsolete items and attach photos when practical. Verify insurance coverage matches replacement values and locations, and check policy expiration dates and special endorsements for fine art, organs, or historic buildings. Document findings and adjust coverage or the register as needed so the church isn’t underinsured at the moment a claim arises.

Reporting Findings And Action Plans

Audit Report Structure And Tone

Organize the report with an executive summary, scope and limitations, findings sorted by area, and an appendix of supporting schedules. Keep tone factual, constructive, and nonaccusatory, focusing on root causes and practical fixes rather than blame. Include enough detail for the finance committee to act, but avoid technical overload for the congregation. Clear, respectful language builds buy-in for change.

Prioritizing Issues By Risk Level

Score findings by likelihood and impact, then present them as high, medium, or low risk so leaders know what to tackle first. High risks might include missing bank reconciliations, large unrecorded donations, or payroll misclassification; medium risks cover procedural lapses; low risks are documentation gaps. Tie risk levels to potential financial, legal, or reputational consequences so the board can allocate resources wisely. Offer timelines aligned to the severity to show urgency.

Drafting Corrective Action Steps

For each finding, list a specific action, the person responsible, a deadline, and measurable evidence of completion. Break large remediation into smaller milestones and assign interim reporting points to the finance committee. Include training needs, policy rewrites, or system changes where relevant, and estimate any costs so leaders can budget. Good action plans move issues from words to accountable results.

Presenting Results To Leadership And Congregation

Start with a closed meeting for the finance committee and senior leadership to review sensitive items, then craft a public summary for the congregation that highlights transparency and improvements. Use plain language, show what was found, what’s being fixed, and how members’ gifts are being protected. Offer a Q and A session and publish the summary with the final report or minutes. Transparency reduces rumor and increases confidence.

Templates, Checklists, And Samples

Church Audit Checklist Download

Provide a concise checklist covering bank reconciliations, offering counts, payroll files, restricted funds, fixed assets, insurance, and minutes. Make it fillable so volunteers can tick off items and record evidence locations. A checklist standardizes audits across years and volunteers, cutting down on missed items and rework. Offer both printable and digital formats for flexibility.

Sample Audit Report PDF

Include a sample PDF showing the preferred layout, language, and level of detail, so leadership knows what to expect. The sample should include an executive summary, findings with risk ratings, a management letter, and appendices with schedules. Templates help smaller churches present professional results without reinventing the wheel. Customize the sample to your governance style before using it for official reporting.

Reconciliation And Journal Templates

Supply bank reconciliation templates that force listing of outstanding checks, deposits in transit, and adjustments, plus journal entry templates with approval lines. Include a schedule for restricted fund reconciliations that ties each balance to supporting receipts and expenditures. Templates reduce errors and make it easy to show auditors the evidence trail. Exportable spreadsheets or integrated reports from your church management app speed this work even more.

Volunteer Auditor Packet

Create a packet for volunteers that includes the audit checklist, sample engagement letter, confidentiality agreement, evidence request list, and a map of records locations. Add quick reference guidance on common tests and how to document exceptions. A well-structured packet shortens onboarding and keeps volunteer auditors consistent and confident. Train volunteers on the packet before they begin fieldwork.

Note: exporting giving and membership reports from a church management app can dramatically reduce manual steps when assembling templates and reconciliations.

Common Pitfalls And Red Flags

Top Finance Mistakes To Avoid

Mixing personal and church funds, skipping monthly reconciliations, failing to document restricted gifts, and weak vendor controls top the list. Small errors compound into big problems, so address them early with simple policies and routine checks. Avoid relying on one person for critical tasks; even small churches need redundancy. Regular spot checks prevent small mistakes from becoming crises.

Fraud Indicators And Warning Signs

Watch for missing receipts, unexplained check payees, altered documents, rapid turnover in finance roles, or unusually large vendor payments to unfamiliar businesses. Repeated late reconciliations and resistance to independent reviews are also red flags. When you see patterns, act quickly with fact-gathering, not accusations, and consider bringing in an external reviewer if concerns persist. Early detection saves money and reputation.

Weak Controls In Small Churches

Limited staff often means poor segregation of duties, single-person control of deposits, and informal approval practices. Compensating controls help, like mandatory dual signatures, rotating cash counters, trustee reviews of reconciliations, and monthly finance committee sign-offs. Use simple written policies and schedule periodic external reviews to add independence. Technology can also help by restricting access and creating audit trails.

Quick Fixes For Recurring Problems

For late reconciliations, set a fixed monthly calendar and assign a backup; for missing receipts, require electronic submission within 7 days; for inconsistent donor records, standardize entry fields and use tags or categories. Small procedural changes, applied consistently, often stop repeat issues. If a problem recurs, log it and escalate to the board with suggested permanent controls so fixes stick.

Tracking Key Metrics After Audit

After the audit you need a simple, repeatable dashboard that shows whether the fixes are working and where new risks are appearing. Focus on a handful of measurable items, review them monthly, and tie each metric to an owner and an action if it wanders. Keep the reporting short, visual, and consistent so volunteers and leaders can spot trends without digging through ledgers.

Monthly Metrics To Monitor

Track only what you will actually review. Typical monthly metrics:

- Total giving, by source, compared to the same month last year.

- Number of donors and number of recurring donors.

- Bank balances for operating, payroll, and reserve accounts.

- Undeposited cash and checks older than 7 days.

- Outstanding checks and credit card balances.

- Payroll expense and headcount changes.

These show cash flow health, engagement, and process lag. Make one page, update it every month, and circulate to the finance committee.

Budget Variance And Cash Ratios

Budget variance tells you whether programs are funded as expected, cash ratios tell you whether you can meet short term obligations. Track:

- Monthly and year-to-date variance, both dollar and percent, for major budget lines.

- Operating cash ratio, current assets divided by current liabilities, to measure short term liquidity.

- Months of reserves, operating cash divided by average monthly operating expenses, to show runway.

Flag variances over preset thresholds, for example 5 percent for major categories or fewer than three months of reserves. When a variance appears, require a corrective action note and owner.

Restricted Fund Balances

Restricted funds must be transparent and reconciled each month. For each restricted or designated fund show:

- Opening balance, receipts, expenditures, and closing balance.

- Source or donor intent, and any legal or grant conditions.

- Unspent but committed amounts, like outstanding purchase orders or pledged program costs.

Reconcile restricted balances to bank accounts and donor records. If a restricted balance drops unexpectedly, document why and what approvals were obtained.

Using Software For Ongoing Oversight

Stop copying numbers by hand when you don’t have to. A church management app that includes giving, member records, and reporting reduces errors and saves time. Use software to:

- Export donor-level giving and deposit reports for fast reconciliation.

- Automate recurring donation tracking and contribution statements.

- Maintain role based access so only authorized people can edit giving or bank records.

- Schedule automated financial reports to the finance committee.

If you can, integrate your accounting system and giving platform so reconciliations become routine, not heroic. That lets your human reviewers focus on exceptions and policy, not data entry.

FAQs

How Much Does A Church Audit Cost?

Costs vary a lot by size and scope. Expect a volunteer internal review to be very low cost, often under $500 in incidental expenses. A CPA review or agreed upon procedures engagement for a small church commonly runs $1,500 to $6,000. A full financial statement audit for a larger or multi site church can be $10,000 to $50,000 or more. Factors that raise cost include complex grant compliance, multiple locations, poor records, or urgent timing. Always get written estimates and compare the proposed scope, not just the bottom line.

How Often Should A Church Be Audited?

Annual review or check makes sense for most congregations. Options to consider:

- Annual internal review or financial oversight by the finance committee.

- External review or agreed upon procedures every 1 to 3 years.

- Full external audit when required by funders, denomination, or when risks rise.

Also schedule an external check when leadership changes, after fraud concerns, or when revenue or operations grow substantially. A rotating schedule, with targeted procedures between full audits, balances assurance and cost.

Is An Audit Required By The IRS?

No, the IRS does not require churches to have an annual financial audit. Churches are exempt from filing Form 990 in most cases, which is one reason audits are not mandated federally. That does not mean you can skip good records. State charity regulators, grantors, lenders, or your denomination may require audits or reviews. Also, the IRS can audit a church for tax compliance, so keep records and controls ready.

What Does The United Methodist Audit Guide Say?

The United Methodist Church provides denominational guidance and tools through its stewardship and finance offices. Typical guidance emphasizes annual financial review, clear segregation of duties, proper handling of offerings, and documented compensation decisions for clergy. Many conferences require either an annual audit or an independent review and offer templates or peer review programs. Check with your conference finance office or district for the specific guide, requirements, and sample forms that apply to your charge.

Can Small Churches Use Internal Reviews?

Yes, internal reviews are a practical, lower cost option for small churches. To preserve usefulness and credibility:

- Use an independent panel if possible, for example trustees or an independent volunteer.

- Follow a written checklist and document all tests and findings.

- Rotate reviewers and require confidentiality agreements.

- Schedule periodic external checks to validate the internal work.

Internal reviews help maintain good controls, but they do not replace an independent audit when external assurance is required.

Where Can I Find A Church Audit Checklist PDF?

Look for checklists from trusted sources:

- Your denomination or conference finance office.

- State nonprofit associations and state charity regulator websites.

- National nonprofit centers or accounting firms that specialize in churches.

Many organizations publish downloadable PDFs you can adapt. Also consider using the downloadable templates found on reputable church finance resources and pairing them with exported reports from your church management software to speed the work.

What Goes In A Church Audit Report Sample PDF?

A useful sample report contains:

- Title, recipient, and date.

- Executive summary with overall opinion or findings.

- Scope, limitations, and level of assurance.

- Financial statements or reconciled schedules if included.

- Detailed findings, each with a risk rating, root cause, and recommended action.

- Management responses and agreed corrective actions with owners and deadlines.

- Appendix with supporting schedules, test samples, and the auditor’s signature.

Keep the sample realistic and concise so leadership knows what to expect.

Who Should Receive The Audit Report?

Deliver the full report to those responsible for oversight and remediation:

- Finance committee and board of trustees or vestry.

- Senior pastor and senior staff.

- Denominational office or grantor if required.

Provide a concise public summary for the congregation that highlights key findings, actions taken, and how gifts are protected. Limit distribution of sensitive attachments, like payroll detail or personnel matters, to those with a legitimate need to know.